Did you know that

8 out of every 10 people

have errors in their credit report?

Start here (in the right order)

First we need access to your reports. Then we run a quick “x-ray” analysis so you know exactly what’s hurting you and what to do first.

1) Start Monitoring

Pick a monitoring option. This gives you scores + report access so we can review what’s reporting and where the issues may be.

2) Schedule a Credit Analysis ($25)

A credit analysis is like an x-ray. We review your reports and give you a clear plan: what’s fixable, what’s next, and what to ignore.

3) Choose a Plan

Pick the level of support that matches your timeline. We focus on accuracy, documentation, and smart strategy—no gimmicks.

Plans (clear pricing, clear expectations)

These plans cover guided dispute/document support and coaching. We can’t remove accurate, timely negative information, and results vary. The goal is to improve your profile the right way—step by step.

Standard

$85 / month

Account setup / first work fee: $150 (one-time)

90-day satisfaction guarantee (terms apply)

- Up to 5 disputed accounts / month

- Standard disputing + factual disputing

- Monthly 1-on-1 check-in

- Chat/email support

- Monitoring not included (additional cost)

Professional

$105 / month

Account setup / first work fee: $250 (one-time)

90-day satisfaction guarantee (terms apply)

- Unlimited disputed accounts / month

- Up to 5 inquiries / month

- Power of Attorney (where applicable)

- Custom disputing + factual disputing

- Monthly 1-on-1 check-in

- Chat/email + text support

- Monitoring not included (additional cost)

Elite

$155 / month

Account setup / first work fee: $400 (one-time)

90-day satisfaction guarantee (terms apply)

- Unlimited disputes and inquiries

- Notarized Power of Attorney (where applicable)

- Custom AI disputing

- Monthly 1-on-1 check-in

- Metro 2 disputing (when appropriate)

- Credit monitoring included

- New credit lines guidance

- 24/7 priority support

Credit services disclosures (read this)

- No guaranteed deletions: we can’t remove accurate, timely negative information.

- Disputes when appropriate: we help identify potential inaccuracies and prepare dispute documentation.

- Results vary: outcomes depend on your profile, reporting timelines, and creditor/bureau responses.

- Your rights: if credit repair laws apply to your service, required disclosures and agreements are provided, including a 3-business-day right to cancel after signing.

Learn more: FTC (CROA) • CFPB guidance

7-Day $1 Trial and then $34.99 per month

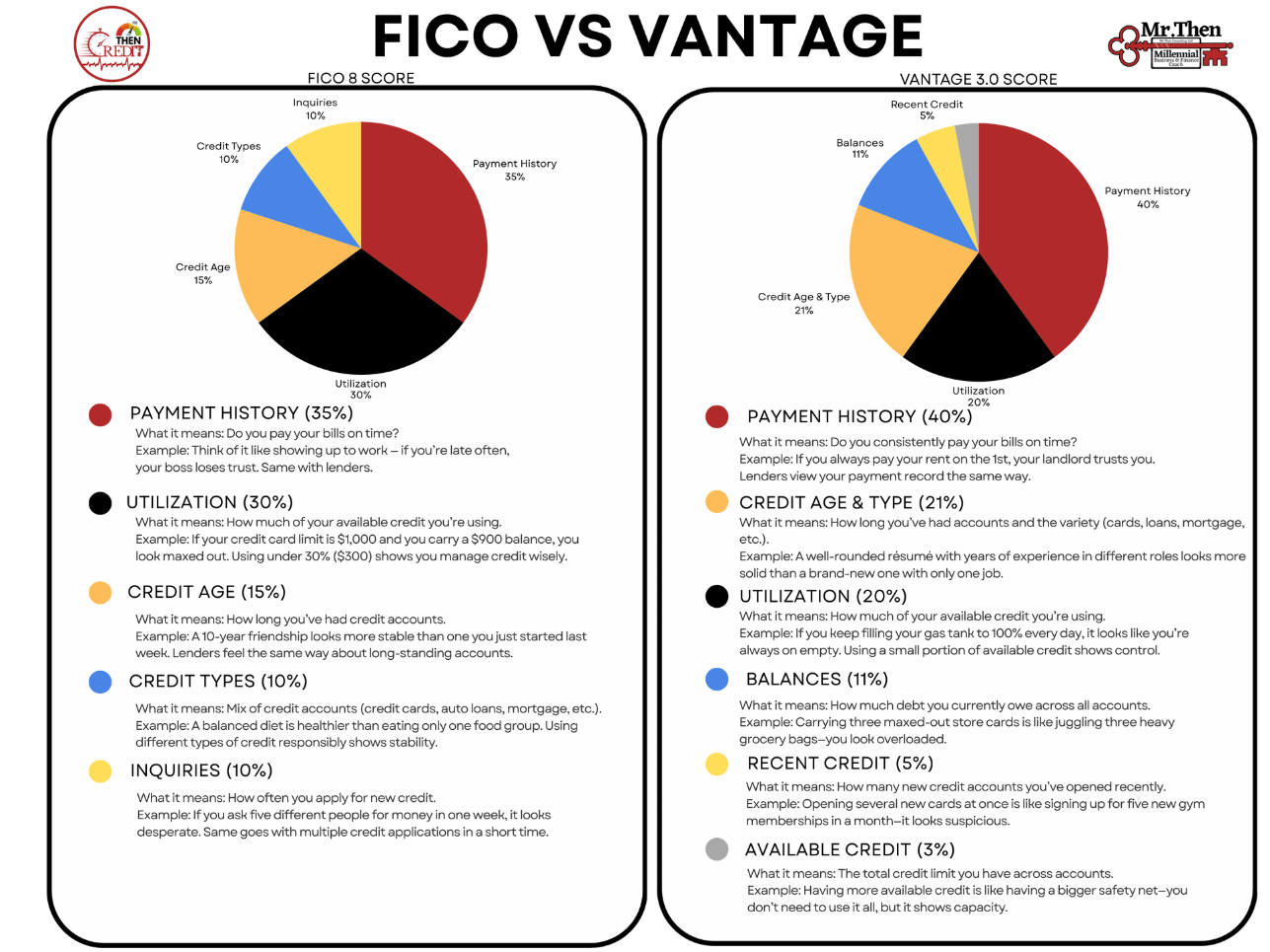

Provides your FICO score which is what Banks Use!

7-Day $1 Trial and then $27.99 per month

Provides your Vantage score which is what the Bureau’s and Credit Karma Show’s.

A Credit Analysis has a Small $25.00 Fee and allows us to see what is going on with your credit like an x-ray. So we can make best possible recommendation.

7-Day $1 Trial and then $51.99 per month

Provides your Vantage score and helps you dispute errors using AI.

Standard Option

$85/Month

Account Setup / First Work Fee:

$150.00 (one-time fee)

Satisfaction Guarantee:

90-day satisfaction guarantee or your money back (terms apply)

-

Up to 5 Disputed Accounts: Assistance with disputing up to 5 accounts per month on 3 Credit Bureaus.

-

Inquiries: Not Included.

-

Standard Letter: Access to pre-designed letter templates for disputing and intervention.

-

Monthly Consultation: One 30-minute meeting per month to review and discuss your credit situation.

-

Factual Disputing: Disputing inaccuracies based on factual errors.

-

Credit Monitoring: Not included.

-

7-Day Trial for Monitoring: $1 trial for 7 days, followed by a monthly fee between $19.95 and $34.99.

-

Online Chat/ Email Support: Response Times within 48 hrs.

Professional Option

$105/Month

Account Setup / First Work Fee:

$250.00 (one-time fee)

Satisfaction Guarantee:

90-day satisfaction guarantee or your money back (terms apply)

-

Unlimited Disputes: No limit on the number of accounts disputed each month.

-

5 Inquiries: Help with disputing up to 5 inquiries per month.

-

Power of Attorney: Includes not notarized power of attorney for dispute management.

-

Custom Letter Templates: Access to customized letters for disputes.

-

Monthly Consultation: One 30-minute meeting per month to review and discuss your credit situation.

-

Factual Disputing: Disputing inaccuracies based on factual errors.

-

Credit Monitoring: Not included.

-

7-Day Trial for Monitoring: $1 trial for 7 days, followed by a monthly fee between $19.95 and $34.99.

-

Email / Online & Text Support: Priority 1-24 hr response time support for quick assistance.

Elite Option

$155/Month

Account Setup / First Work Fee:

$400.00 (one-time fee)

Satisfaction Guarantee:

90-day satisfaction guarantee or your money back (terms apply)

-

Unlimited Disputes and Inquiries: No limit on the number of accounts or inquiries disputed each month.

-

Notarized Power of Attorney: Includes notarized power of attorney for efficient dispute management.

-

Custom AI Letters: Access to custom AI-generated letters for precise and effective disputes.

-

Monthly Consultation: One 30-minute meeting per month to review and discuss your credit situation.

-

Factual Disputing: Disputing inaccuracies based on factual errors.

-

Metro 2 Disputing: Advanced disputing Creditor Industry Standard method for more complex credit issues.

-

Credit Monitoring: Included (Vantage Score 3.0)

-

New Credit Line Assistance: Help with applying for new lines of credit to improve credit profile.

-

24/7 Support: Priority support available 24/7 for urgent inquiries.

Pay Per Item Dispute Support:

Account Setup / First Work Fee:

$250.00

NO MONTHLY FEES

$0/ Month

Email Support: Response Times within 48 hrs.

7-Day Trial for Monitoring: $1 trial for 7 days, followed by a monthly fee between $19.95 and $31.99.

Pay as you go per Bureau per Item/Account

$0.00 Per Personal Information

$5.00 per Inquiry

$50.00 per Collection/Charge off, Student Loans, Tax Liens, Repossessions, Evictions,

Foreclosures/Child support , Bankruptcies/Civil Judgments, Anything Else

Do it Yourself Option:

Account Setup / First Work Fee:

NO FIRST WORK FEE

$0.00

$50/Month

Credit Monitoring: Included in the fee.

View your 3 Bureau Reports

Dispute Unlimited Items at your Pace

AI Assisted Dispute Process

Cancel at ANY time